BASED OF THE UNDERSTANDING OF FISCAL & MONETARY POLICY, THE REPORT SUGGESTS HOW THESE POLICIES ARE TYPICALLY USED DURING THE DOWNTURN AND CAN THEY BE CONTINUED WITH TO UNFOLD THE GLOBAL ECONOMIC CRISIS? ALSO, WHAT IS THE NEEDFUL AT THIS HOUR OF EPIDEMIOLOGICAL CRISIS?

Impact on varied arenas have been located:

1. GLOBAL STOCK

Barely anyone laments the end of the initial 2020 quarter to engage fear of a U.S.- Iran war offered route to the covid-19 pandemic which had driven the world economy into a 12% contraction over January-March. The quarter saw the most fierce worldwide value breakdown since the Great Depression, exacerbated by a 60% oil value drop. April might not bring a lot of help, with the virus as yet spreading exponentially and keeping enormous pieces of the worldwide economy covered.

2. PREVALENT PAYROLL

Through decades of low economic growth and inflation, the brightest spot was unemployment rate in U.S. going low, though that boom got ended by the advent of covid-19. With infection surging cities into lockdown and businesses into shutters, people filled over 3 million unemployment benefit claim over a period of February and March, with loss of job for over 293,000 labor force, the largest drop in last few decades.

3. CHINA’S CADMEAN VICTORY

With the world factory opening, the market is closed and the shoppers are gone. China’s social isolation policy might have contained the virus within controllable limits, also allowing its export market to close. It is hence neither getting the imported items it needs nor demand for its products. Jan-Feb profits have been the lowest ever experienced by them in the last decade upcoming manufacturing surveys also reveal more pain. And similar to other nations, it is also expected to suffer a -2% growth in the next 3 years.

4. EURO CENTRAL BANK

The European Central Bank has already massively increased its asset purchases and more flexibility on share of bonds and buffered cost of euros. Such aggressive steps are taken to contain the economic effect of covid-19 and also to stabilize the capital market yet it is expected to shrink the euro economy by 9% by the end of this year.

5. FINANCIAL SECTOR (EXPECTED IMPACT)

BANKS PROFITABILITY WILL BE UP FOR AN EXPLICIT PRESSURE:

• The speculative impact of purchase will affect consumers’ decision making power to borrow loan from banks which will create low credit creation under recessionary market

• This will increase the burden of credit and excess reserve collection for banks post the moratorium period due to the lock down

• Further the difference between the interest generated by banks and the interest paid out to their lenders also get depressed i.e. the Net Interest Margin (NIM) is ruptured eventually.

NIM = (Interest Received – Interest Paid)

__________________________

Average Invested Assets

If NIM gets affected and starts to decline it will also affect Net Average Invested Asset Value in a negative note.

• The dominant restrictions on cross border trade will also cause hindrance in mobilizing monetary transactions among consumers which in turn will case less currency in circulation, one of the most prominent facts of M1(India) is up for a toss.

• The volatility of the capital market will induce imbalance in equilibrium of distribution of wealth affecting mostly on the deprived class of people who are most valid for the lower ranks of the banking cluster.

LIQUIDITY OF THE ASSETS:

• Liquidity of financial institutions may be recovered by RBI’s current alteration in CRR and Marginal Standing Facility Services. However, this will not affect the private, co-operative banks or the Smaller Sections of the financial sector due to the customer’s ‘Flight to Safety’ propaganda which induces fear to invest or to borrow currency from banks.

• Uncertainty of recovering from the moratorium creates a potential credit-loss effect on the banks towards securing risks on monetary bills and bonds causing a negative impact on the fund raising capability of the financial institutions.

• Repayment of term loans and other credit facilities earlier pursued also comes with an ambiguity at this hour for banks who are already suffering from predominant pressure of debt.

IS THIS A TEMPORARY PHENOMENON OR AN INDICATOR OF STRUCTURAL TRANSFORMATION UNDERWAY?

IF SO, TRANSFORMING INTO WHAT EXACTLY?

EFFECTS & ANALYSIS OF THE NEW MACRO POLICIES

At first, COVID-19 looked like a Supply shock:

1. Disruption in Global Chains

2. Quarantine already caused fall in Labor Supply

Then, Demand drawback materializes due to the following reasons:

1. Uncertainty of the pandemic outbreak

2. Uncertainty about the performance of the economic policies

3. Probationary workers losing their jobs especially those in the manufacturing industries

4. Household increases precautionary savings due to speculative mode of demand and thereby firms lose liquidity in investments.

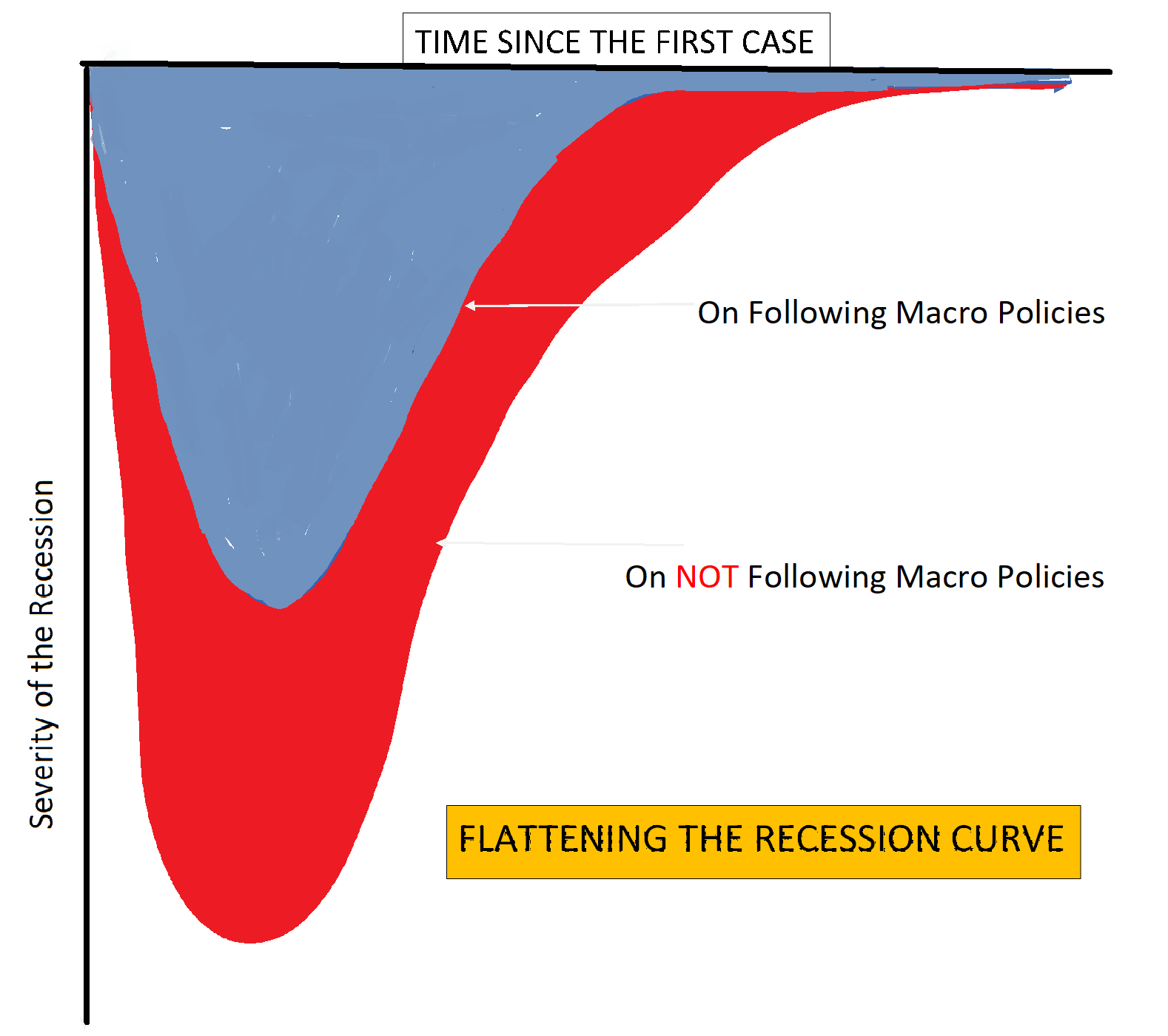

WHEN THE WORLD FALLS APART, POLICIES NEED TO:

• Start from Health Expenditure where investments are to be procured in testing and expansion of medical supplies. Though it is too late now from Stage 1 & 2, yet still time to contain the 3rd & 4th peak in the fall of 2020.

• In case of Cash Disbursements to households and businesses Tax incentives, tax cuts, emergency loans and borrowings are to be encouraged to prevent the collapse of Aggregate Demand and precautionary saving index from rising.

• Using Fiscal & Monetary Interventions in Co-ordination to maximize and impact the economy, proving it the fullest financial backing at this hour of epidemiological crisis.

All Comments () +